China’s Threat to Ban Critical Mineral Exports Is Not a Bluff

Editor's Note

This story originally ran on July 23, 2024. With China's decision to block exports to the U.S. of key semiconductor chipmaking materials, we have decided to re-run the article to offer more context on the trade threats for electronic components.

Over the past year, China has imposed export controls on gallium, germanium and graphite—all critical minerals necessary in important downstream goods like semiconductors. As U.S.-China competition intensifies, it’s a real possibility that China could implement further controls—even bans—on mineral exports to the United States.

As the six following points explain, China’s threat to ban critical minerals exports is not a bluff, and such bans could create mineral shortages in the United States.

Point 1: China has previously implemented export restrictions and bans. In articles published in the Chinese Communist Party’s Global Times and with visits by President Xi Jinping to rare-earth facilities, China is signaling that it may impose consequential export controls on minerals. The precedent is there: China blocked rare earth exports to Japan in 2010 and banned exports of rare earth processing technology in 2023.

Point 2: China could benefit from imposing mineral export bans. Export bans on select minerals would demonstrate that China can retaliate against U.S. efforts to curb technology exports to China—and possibly deter the United States from further restrictions, enabling China to stock up on U.S. technology.

Point 3: Chinese mineral producers could likely find alternative customers to the United States. China mines 70% of the world’s rare earth elements but consumes more than 80%. In many cases, China is the largest consumer of its own critical minerals. In fact, China’s demand for many critical minerals is so high that it relies on imports to meet substantial portions of its domestic consumption.

In addition, some developing regions like Southeast Asia have increasing mineral demand from their growing manufacturing sectors that China’s mineral producers could tap into.

Point 4: China dominates production of many critical minerals. EU countries were able to move away from Russian natural gas dependence in response to its invasion of Ukraine, but China’s dominance of the critical mineral industry is far greater than Russia’s influence on the natural gas industry. Russia is the world’s second-largest producer and exporter of natural gas, but it has less than a 20% share of global gas production. China, however, in 2022 was the leading producer for 30 of the 50 minerals on the U.S. critical minerals list, and it had a majority share in global production for many of these minerals. Thus, the consequences of China cutting off critical mineral exports to the United States are likely broader and more severe than Europe dropping Russian natural gas exports.

Point 5: The United States and its partner countries likely cannot quickly produce enough minerals to fully replace imports from China. After Russia cut off natural gas to Europe during the Russia-Ukraine war, European countries switched to largely importing natural gas from existing liquified natural gas export terminals in the United States and other countries. In critical minerals, the situation is different. The United States could turn to existing mineral producers in partner countries like Australia and Canada, assuming those mineral producers have excess production to sell. Yet for many minerals, especially those necessary in electric vehicle batteries, mineral producers sign long-term offtake agreements—some up to 10 years in duration—with downstream customers. Therefore, many producers have already committed large portions of their production to customers for several years and lack significant excess production to sell to other customers. And for those mineral producers that seek to expand their production capacity, they would need several years to build new mines and processing facilities given development and permitting timelines. Consequently, a Chinese mineral export ban may boost mineral collaboration among the United States and its partners, but it does not guarantee that extra minerals would be available to meet their collective demand.

Point 6: The United States would struggle to incentivize enough mineral production in resource-rich countries outside China. To help satisfy U.S. mineral demand, the U.S. government could financially support critical mineral projects in resource-rich regions like Africa and Latin America, as China does. But money alone may not spur mineral producers to build mining and processing facilities in mineral-rich jurisdictions with investment risks like royalty disputes, ethical concerns and regulatory issues. Conversely, Chinese companies are often willing to work in such environments. Therefore, offering U.S. capital for critical mineral projects in resource-rich countries does not ensure that mineral projects will be built there.

How Should the U.S. Address This?

To mitigate the risks of potential Chinese export bans in the short term, the U.S. government should increase its mineral stockpiling. If China imposes mineral export bans, the U.S. government could sell stockpiled minerals to key U.S. industries like the defense industrial base by declaring a national emergency, which is a statutory requirement for releasing minerals from the National Defense Stockpile. Currently, however, the stockpile is only around 1% of its 1962 value.

For instance, the National Defense Stockpile only has 836 short tons of nickel, which is less than 5% of the Department of Defense’s annual nickel usage. And the stockpile does does not presently contain any of the four minerals used most by the Department of Defense: aluminum, copper, lead and fluorspar.

The prices for many minerals have declined over the last two years, making the present a propitious time to increase the mineral stockpile, especially with global shortages of some minerals forecasted by the end of this decade, even without a ban.

In addition to stockpiling, the U.S. government could offer low-cost financing to U.S. companies to secure long-term offtake mineral agreements with trusted providers in the United States and partner countries like Canada and Australia. Major US consumers of minerals like automakers are already pursuing long-term offtake agreements for minerals such as lithium. Concessional financing would further encourage this.

Such actions will incur additional costs, yet companies may view such costs as acceptable for a resilient supply chain compared to the potential costs of mineral shortages.

To mitigate the risks of potential Chinese export bans in the long term, the U.S. government should increase funding for mineral exploration, including drill programs to locate and define mineral resources as well as technical studies to evaluate the project.

Exploration is key for increasing the U.S. mineral supply and decreasing reliance on China. Under Title III of the Defense Production Act (DPA), the U.S. Department of Defense is funding some mineral exploration efforts, including nickel exploration in Minnesota and cobalt exploration in Idaho. Title III also allows the department to fund mineral exploration in Canada, Australia and the United Kingdom, as those countries are considered “domestic sources.”

The US government should also further increase funding for mine exploration and development. Developing a deposit into a producing mine can take billions of dollars and several years. Therefore, a low cost of capital is vital.

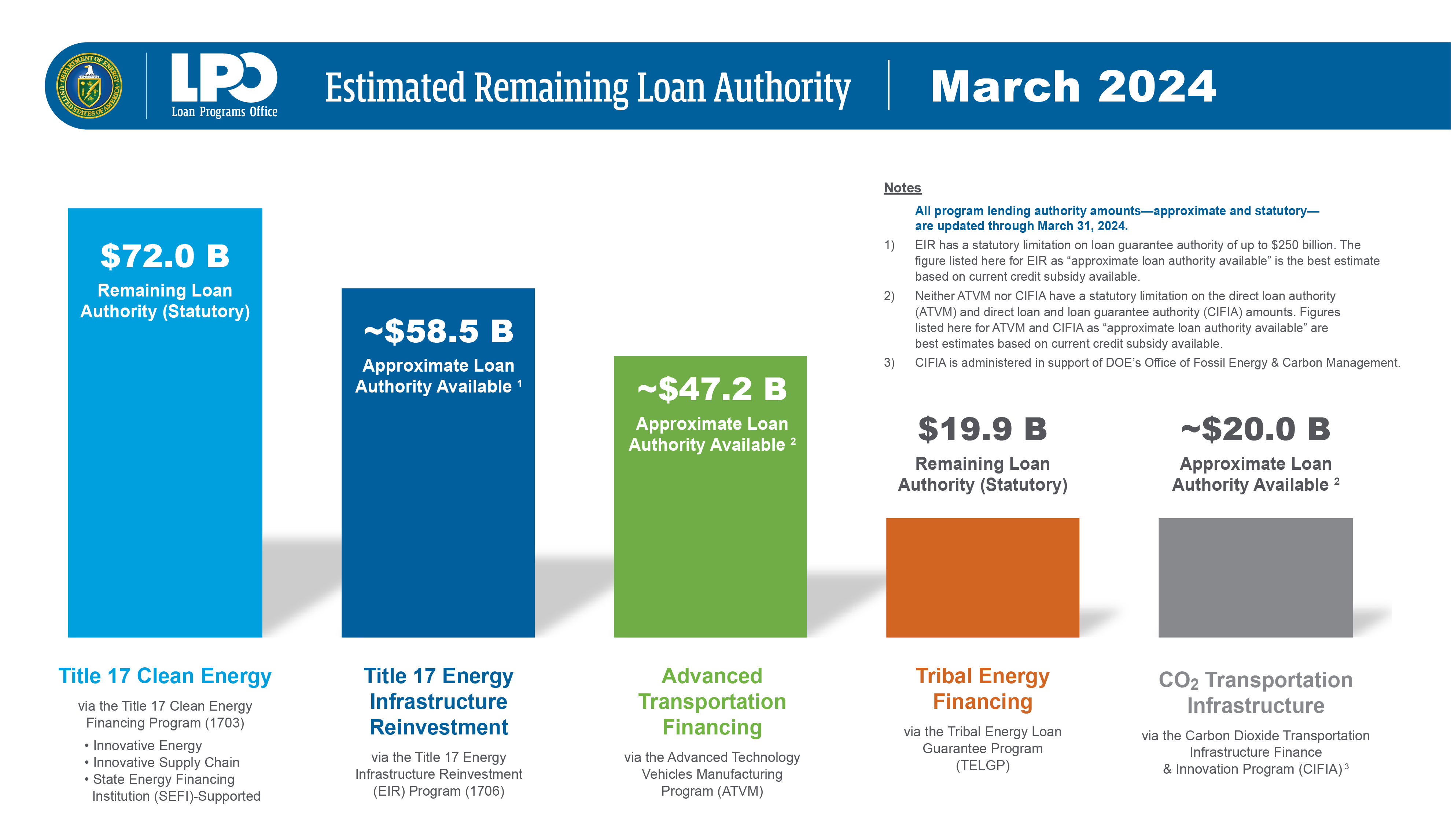

So far, the U.S. government has offered neither grants nor loans for domestic mine development, although it is offering substantial grants and loans for mineral processing. Importantly, the US Department of Energy’s Title 17 Clean Energy Financing Program can indeed support the development of domestic mines, as it is authorized to provide nearly $72 billion in loan guarantees to eligible projects, which as of April 2024 include mineral extraction projects.

{kind=link}

The U.S. government and U.S. companies should recognize that China’s threat to ban exports of critical minerals is not a bluff—and take the threat seriously by stockpiling minerals, developing mineral supply chains excluding Chinese companies, conducting mineral exploration, and funding mine development.

About the Author

Gregory Wischer

Non-Resident Fellow, Payne Institute for Public Policy

Gregory Wischer is a non-resident fellow at the Payne Institute for Public Policy at the Colorado School of Mines. He is also a non-resident fellow at the Northern Australia Strategic Policy Centre at the Australian Strategic Policy Institute.

Lyle Trytten

Independent Consultant

Lyle Trytten is an independent consultant and a 30-year veteran of the mining and metals processing industry, with a focus on responsible development of the metals required for the energy transition, especially nickel and cobalt.